Focus On This Macro Data

Investors,

The majority of market participants still misunderstand the macro environment.

They keep citing cracks in the labor market, rising default rates, the consumer’s dependency on credit card spending, and an increasing whirlwind about private credit.

But we need to focus on the things that actually matter.

Because the fact is that we are not armchair economists.

We are not here to pontificate about policy or to magnify niche data.

We are investors, trying to make money in the market via arbitrage.

It’s why, despite having a degree in economics, I often say that the majority of investors need to ignore macroeconomic data because of the fact that the stock market is NOT the economy (I just talked about this topic last week).

Most investors fail to understand this basic point…

The economy doesn’t need to be good/strong in order for the bull market to stay intact.

The economy only needs to be good enough to support the ongoing bull market.

It’s the same reason why stocks don’t bottom on good news…

They bottom on less worse news, once the market determines that there’s more bad news in the rearview mirror than the potential for bad news on the road ahead.

If you don’t believe me, just look at the ongoing rally since the March 2026 lows.

The Nasdaq-100 has gained +33% in these past two months, and yet:

There is no peace deal

The Straight of Hormuz is closed

There is potential escalation with Cuba

Inflation is reaccelerating at a meaningful pace

Consumer confidence is making new all-time lows

Risks are still present, we’d all agree.

But one of the key things that I’ve learned in my 13-year career is this…

Risks are ALWAYS present.

If you’re waiting to invest (or only willing to stay invested) until you see a sign from the heavens that there are no more negative catalysts coming down the pipeline, I wish you all the best.

Instead, we need to recognize the following:

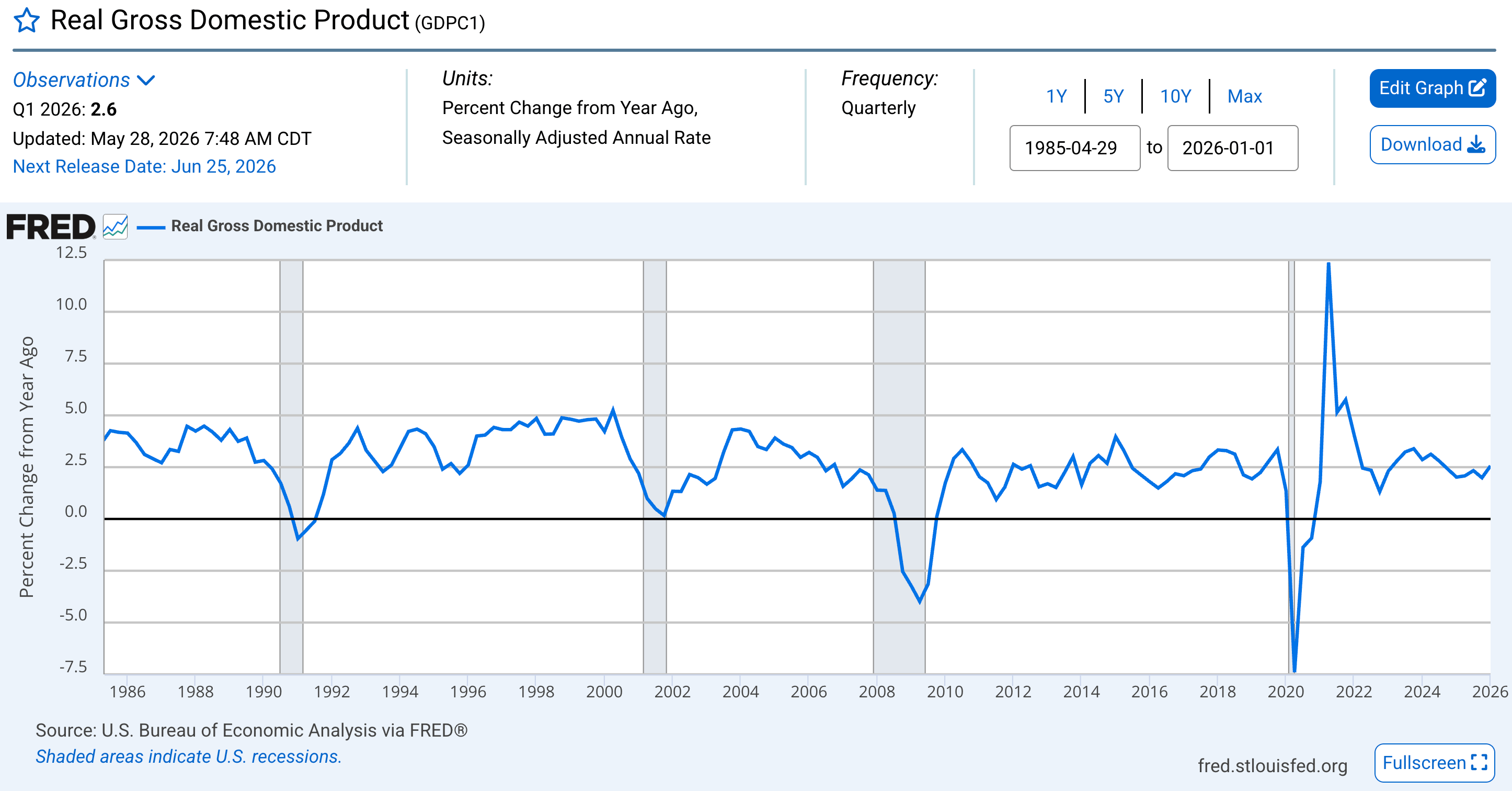

Real GDP growth for Q1’26, while revised lower from the initial estimate of +2.0% quarter-over-quarter annualized, came in at +1.6% annualized growth.

This isn’t going to knock anyone’s socks off… but it’s still indicative of an economic expansion, even after adjusting for inflation.

But as we’ve discussed in the past, I’ve always believed that QoQ annualized growth is a flawed metric and I actually prefer to analyze real GDP growth on a YoY basis.

When we use this lens, we see the following:

Real GDP growth in Q1’26 was +2.6% YoY, a notable acceleration vs. the YoY growth rate in Q4’25 of +2.0%.

Additionally, does this reacceleration look anything like the environment that preceded the recessions in 1990, 2001, or 2008?

Absolutely not!

In fact, the growth trajectory for real GDP looks more reminiscent of the choppy (but stable) oscillation coming out of the Great Recession, from 2010-2019.

Throw in the fact that Redbook retail sales jumped to +9.0% YoY, showing that same-store consumption is growing at an epic pace.

Yes, this +9.0% figure is nominal, but I found this super interesting…